With the stock market reeling, thousands of people losing their jobs, and Marion County’s unemployment at an 18-year high, Ocala Style magazine had many questions about what still needs to be done. Was the bailout a good idea? Has the housing crisis hit the bottom? What can average consumers do to protect their hard-earned money?

We figured the best way to get the in-the-know answers was to gather a hand-picked group of top banking officials together to ask them all these tough questions face to face. Over a two-hour luncheon in a private room at the Country Club of Ocala on a beautiful autumn morning, Publisher Kathy Johnson and Editor-In-Chief Dean Blinkhorn hosted a unique forum where the camera was clicking and the tape was rolling. Here’s what everyone had to say.

THE PARTICIPANTS

Dean Blinkhorn—Editor-In-Chief, Ocala Style Dave Fechtman—Market President, Wachovia

Roy Hilgenfeldt—City President, Compass Bank Mark Imes—President & CEO, Independent Na. Bank

Tom Ingram—CEO, Gateway Bank of Central Florida Kathy Johnson—Publisher, Ocala Style

Chris Yancey—Market President, Mercantile Bank

‘Most Of The Banks Are Still Solvent’

Dean: Let’s start with the bailout because that’s what’s on everyone’s mind right now.

Tom: I don’t know how these guys feel, but there’s a lot of anger toward it. I personally prefer it just because there’s fear with the market. It does have a big effect on Main Street—this could be catastrophic if we don’t step in like we’re doing.

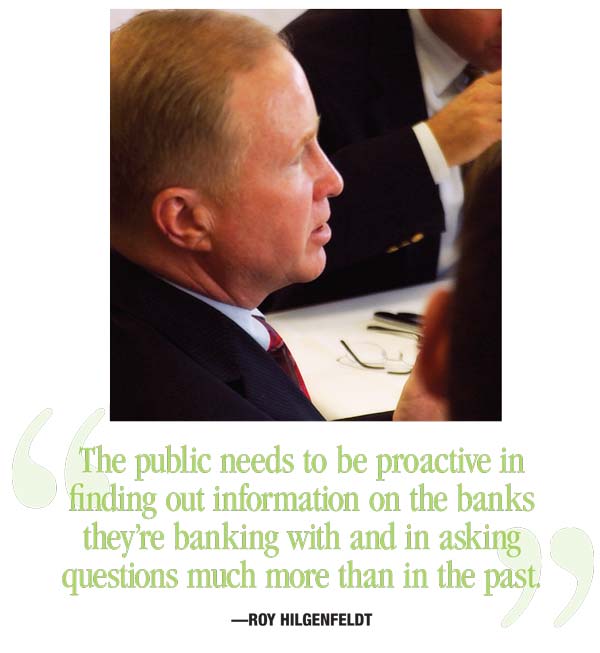

Roy: It’s important for consumers to recognize that most of the banks within the United States are still solvent—not every bank needs to be bailed out. The public needs to be proactive in finding out information on the banks they’re banking with and in asking questions much more than in the past.

Dean: What do you think it means to the average consumer?

Chris: I think one of the biggest misconceptions is that this bailout is for the rich stockholders—that’s not the case. If something doesn’t happen, there’s going to be a loss of jobs in the financial sector. And then we’re not going to be making loans, and if we don’t make loans, other sectors of the economy will start losing jobs because the economy won’t be able to grow. Businesses won’t be able to fund their projects, and it will trickle down.

I heard a great analogy: If you think of the economy as a sprinter, the sprinter has fallen and is having a heart attack. Somebody’s got to intervene or the sprinter’s going to die. That’s really what’s happened to the whole financial sector—it’s stopped and somebody’s got to do something.

This isn’t the best plan, but we need to intervene now to make something happen. It will trickle down.

Roy: If consumers aren’t confident in their economy, then they’re not spending their money, they’re saving. The economy is not only going to not grow, it’s going to shrink. It’d be a snowball effect.

Mark: Ninety-five percent of the problem is fear, which is preventing the markets from working the way they should and is driving people to protective behavior. This will help them get back into behavior where banks will lend to banks again.

Roy: And the fear shows. What they have to do is stop this fear.

Dave: The lending has not come to a screeching halt, but it’s far from a sprint, to use Chris’ analogy. I’m sure all of us are being very deliberate in who we lend to.

Tom: You’re going to have to actually qualify for the loan and show that you can repay it. That’s what was missing before. We’re getting back to good ol’ fashioned banking the way it should be.

Kathy: So it’s a little bit of a reality check…

Tom: It is, but we needed it. I think banks will still continue to lend money—it’ll be tough for a while because everybody’s licking their wounds—but we’ll survive this and get back to business as usual.

Dave: People think only troubled businesses are failing or struggling. I think we could all look at our portfolios and say our strongest clients are struggling right now. If we’re unable to help them with their cash-flow cycle, people become unemployed.

And we’re not just talking about certain industries that are obvious, but really across the board. Things are getting difficult for almost all industries, even medical and some folks that we believe to be recession-proof. It’s a big deal.

Mark: If I’m going to buy a house and I’m putting 20 percent down and I’ve got good credit, I can get the mortgage just as easily as I could a year ago. In fact, I’m going to get the mortgage today at a lower interest rate than I did a year ago. Does anyone disagree

with that?

All: No.

Mark: In fact, we’ve done more mortgages this year than we did the year before. But we’ve always required down payments. The money is out there.

I think some of this is overstated. But, yes, there are segments where people can’t borrow. If you think it’s a great time to do a spec house, I’m probably not going to finance that.

Mark: We were fostering more of that than we should have a couple of years ago.

Roy: A lot of people were buying second and third homes and taking advantage of the lack of an equity requirement, all on the anticipation of not really holding these homes long-term. They thought this great increase was going to continue indefinitely. All of a sudden, that avenue evaporated and they were stuck.

Dean: And the banks don’t want the homes.

Chris: If we take it back, we’re going to lose money—guaranteed. We don’t take back properties or equipment and end up making money.

Roy: By the time it gets to the borrower letting the bank take their property back, you can bet that’s not a good situation. There’s not going to be equity.

Dave: Everybody loses.

‘No One Really Did Enough’

Dean: What can Marion County do, since it’s relied so heavily on the housing industry?

Mark: Historically, you’ve been able to overcome a divorce or a loss of job—these things happen—because your house could sell at a profit. Now, those ordinary life events that people used to be able to solve with the sale of a house can’t happen because we’ve got a three-year inventory on the market.

Dave: Those are heart-wrenching. The human element of this is something Congress has to remember. It’s not just a bank issue.

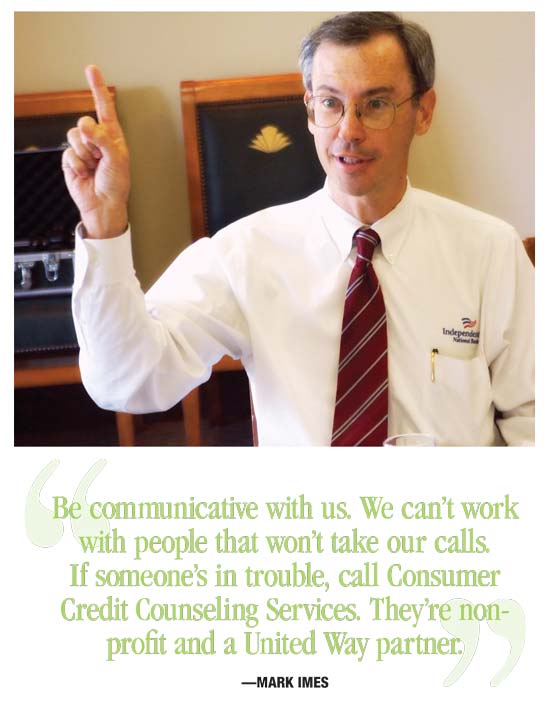

Mark: One thing is to be communicative with us. We can’t work with people that won’t take our calls. Is that common for everybody?

All: Yes!

Dean: So if someone loses a job, you guys are the first people to call. They shouldn’t hide, right?

Chris: Yes, and before they get three or four months behind.

Mark: We’ve done payment plans for people like that.

Roy: Don’t wait until the problem is so severe that we’re not able to come up with a plan.

Kathy: I think that’s an important message to get out.

Tom: The person looking to make the payment, those are the types of customers that a bank can work with.

Dave: The by-product is more responsibility. Do some things now to prevent getting into that scenario. For folks on a fixed income, be a little bit more deliberate about your finances and your budgeting. Folks that aren’t on a fixed income, give yourself a little bit of a buffer today, so that if the worst-case scenario happens 12 months from now, you’re not in

dire straits.

We’re trying to educate the community on financial literacy. I think it’s really important right now to go to the root of the problem and try to fix it before it continues to

get worse.

Roy: At the time, no one really did enough to educate those consumers as to what they need to do from a financial budgeting perspective. It’s a big decision. They need to be prepared for having to make these payments in the future, and they need to have a handle on their finances to make certain they’re going to be able to achieve that. I don’t think that was done very effectively. I think people just went in with the dream of having that home with the picket fence.

Dave: And the plasma TV.

Chris: When you look at the foreclosures in Marion County, it’d be interesting to see how many of those have people living in them. Most of the foreclosures are homes that were investments, not for someone to live in.

Dean: There are certain neighborhoods in Marion County that have been harder hit than others.

Chris: Yeah, but a lot of the people making it boom were investors from outside of Florida.

Roy: Paying exaggerated prices. In many instances, double what the developer was initially thinking of getting. Then someone else would come along and pay even more.

Tom: In some cases, they’d say, “That’s a great deal. Give me three.”

‘Read The

Fine Print’

Dean: Let’s talk about personal responsibility. What should people do?

Dave: If your employer offers direct deposit, have them put a percentage directly into savings.

Roy: Create a cushion.

Dean: What would you recommend a cushion to be? What portion of someone’s salary?

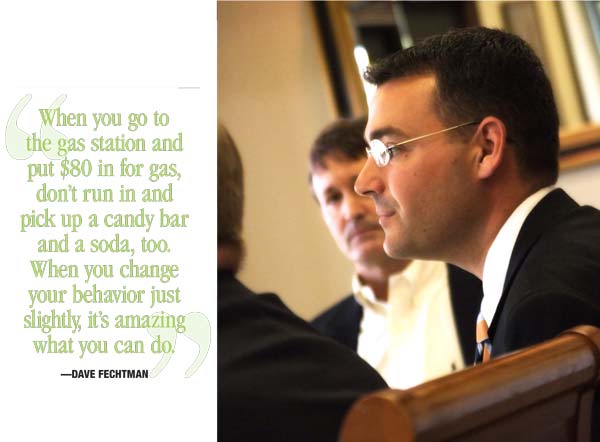

Dave: That’s challenging right now. What most people don’t realize is even if it’s $25 a paycheck, you learn to adapt your lifestyle to live within those means. When you go to the gas station and put $80 in for gas, don’t run in and pick up a candy bar and a soda, too. When you change your behavior just slightly, it’s amazing what you can do.

Roy: Once you have a budget, you develop a lifestyle. A lot of things that you might say are necessities really are not. You need to be conscious of what’s a luxury.

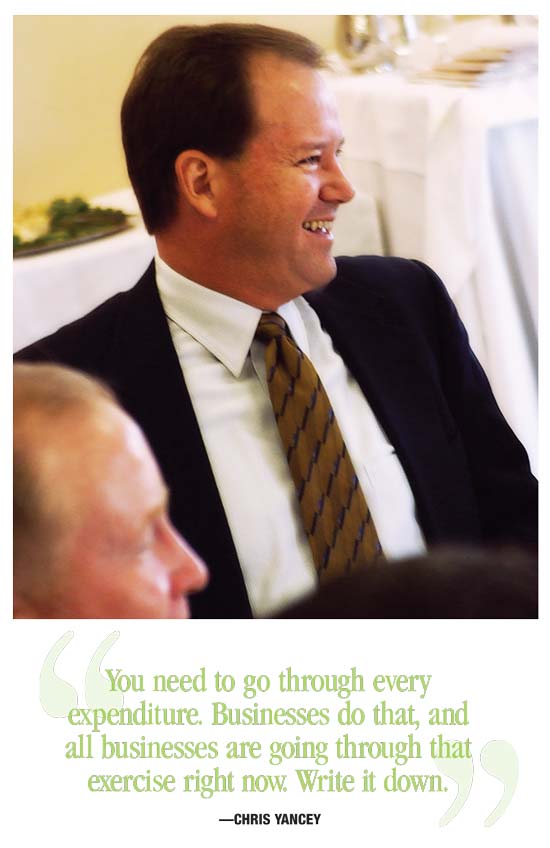

Chris: Roy makes a good point about a budget. It’s a very simple formula—you’ve got a certain amount of revenue and you can’t spend more than that. You need to go through every expenditure. Businesses do that, and all businesses are going through that exercise right now. Write it down.

Dave: I’d recommend that your readers sit down with their banker and come up with a plan that will give them a compass. Then it’s their job to go out and execute it.

Mark: If someone’s in trouble, call Consumer Credit Counseling Services. They’re non-profit and a United

Way partner.

Dean: So people should steer clear of any for-profit credit counseling services?

Dave: Or a check-cashing business and a high-interest loan on their paycheck. Those are things they need to be really cautious about.

Roy: In tough times, you don’t want to become credit card-dependant. Too many people don’t realize how long they’re going to be paying for that item. Understand the rules before you go into something.

Mark: Read the fine print.

Dave: There’s an epidemic going on nationally where people are worried about banks not lending anymore, so they’re racking up their credit card debt and their equity lines intentionally to put money in their mattress for a rainy day. It’s exacerbating this whole situation and spiraling out of control.

Roy: But the important thing for people to remember is that banks need to loan money to make money. We need our community to grow for us to grow. The last thing that any of us at this table want to do is to quit loaning money. We’re all here to continue to support the growth of our communities.

‘A Safe Place For Your Money’

Kathy: If people can afford right now to pay off their mortgage, should they?

Tom: That’s a very good question. You have to look at the whole picture.

Roy: They should seek out qualified financial advice that the banks offer.

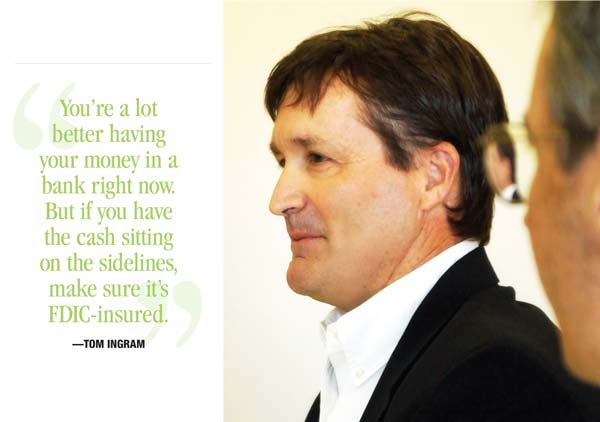

Tom: I think you’re a lot better having your money in a bank right now. But if you have the cash sitting on the sidelines, make sure it’s FDIC-insured.

Roy: No one has lost money from FDIC-covered deposits.

Kathy: They just raise the amount of money that FDIC will insure to $250,000, right?

Chris: That’s an important point.

Roy: I think that’s good at this time. Economic conditions have changed.

Chris: I absolutely agree. The dollar today is not a dollar from 50 years ago. It’s important that people understand that the FDIC has always covered what they were supposed to cover. Nobody has ever lost any money from FDIC insurance.

Dave: That is really, really important.

Roy: It protects not only individuals, but small business. The average individual might say, “I’m not ever going to have over $100,000 where I have to worry about the FDIC insurance.” But a small business does. That’s their business capital. That’s supporting their company, their employees, and the products they need to buy and the timeframe till they sell. You’re protecting small business by doing this, and small business is the heart of this country.

Dave: And folks think they need to spread their deposits over 20 institutions to protect themselves. But almost every bank has solutions to get FDIC coverage.

Kathy: Well, I thought you all would want to talk about that. It’s a type of insurance, but a larger amount, right?

Roy: You can essentially provide coverage up to $50 million to one account. CDARS (Certificate of Deposit Account Registry Service) is the name of the program, a network of about 1,800 banks that participate and reciprocate CDs. It’s a nice way to have all your eggs essentially in one basket.

Tom: Let’s back up a little bit and talk about the FDIC insurance because I think that’s very important now. It’s a safe place for your money and has been around for 75 years. It works.

Mark: It’s an insurance fund, not taxpayer dollars. This is something our industry does in conjunction with our regulators.

Chris: And we pay very high premiums for that insurance.

Mark: We pay $150,000 a year, and we’re just a flea on the tail of a dog.

‘Tell The

Entire Truth’

Kathy: What would you recommend for seniors to do right now with their money?

Dave: Go talk to their bank or investment advisor, someone that they’re comfortable with. There are solutions to help them.

Roy: There are so many investment options and mistruths out there. The worst thing to do is to not seek advice.

Dave: Or to panic.

Chris: When you seek professional advice, just like going to the doctor, you’ve got to tell them the entire truth. Many times we have clients come in who will say, “I’ve got $100,000. What should I do with it?” Well, what else do you have?

You’ve got to reveal the whole story to your professional advisor—whether it’s a banker or a broker—because we don’t want to mess up an estate plan or some other type of savings.

Roy: That’s a good analogy. The key is always diversification—keeping things in safe investments and knowing your risk level.

Kathy: Well, seniors shouldn’t be taking too many risks, right?

Roy: No. Usually when you get to the point of retirement age and you’re on a fixed income, the last thing you need to do is increase your risk tolerance.

‘We’ve All Learned A Lesson’

Dean: Let’s get back to the local level. Now that the bailout has passed and the FDIC level has been increased, how is that going to affect local businesses?

Dave: There is a tremendous amount of talent in Marion County in the banking community. I think we’re all still lending money. I haven’t heard of one bank in town that’s not making loans.

Chris: I think we’ve all learned a lesson over the last couple of years with easy credit. We’re all documenting better than we used to. The way we all came up in banking, you didn’t make a loan until you knew a lot about a customer. Everybody got away from that because money was flowing and equity was going up.

One thing consumers need to understand is that we’re still making loans. We’re just asking a lot of questions, but no more than when I was with Barnett Bank 15 years ago.

Dean: How has banking changed in Marion County?

Chris: The more it changes, the more it stays the same. You’re always going to have really big banks and local independent banks. It depends on what you need.

Dean: Do you see banking coming back to a more one-on-one, personal level?

Dave: If we were in Miami or something, you could probably say that. But in Marion County, we know our clients.

Mark: It’s interesting. I started at Barnett Bank in ’85 and Chris was already there. We saw this in Marion County in ’90 and ’91 with all the S&Ls defaulting. I think we were probably tighter in ’91 than we are right now. We shut it off in ’90 and ’91. I mean, we shut it off.

Roy: Well, interest rates were skyrocketing. But we managed to work through it, just like we’ll manage to work through this situation.

Dave: The underlying messages we’re talking about—being more responsible, partnering with your bank, being proactive—those are the things that matter, those are the things that readers should take away.

‘Get Rid Of

The Fear’

Dean: In every economic downturn, there are also economic opportunities. Let’s talk a little bit about that.

Chris: You have to remember that the one thing we have that much of the country doesn’t have is sunshine. And our land, even though it’s elevated, is still much cheaper than most of the country. The other thing we’ve got is The Villages in our backyard. Those things will continue to fuel us, on top of a great economy that’s very diverse—mobile home manufacturing, horse farming, light manufacturing, and a great medical community.

Roy: People don’t come here to buy a house; they come here to buy a lifestyle. We have a very unique lifestyle, and that hasn’t changed, despite our economic climate.

Dave: I think buying local will help with the recovery.

Tom: I’m glad you said that because everyone needs to be doing that. The opportunity to buy a house in Marion County has never been better. Builders are discounting 30 percent off their cost in very nice areas. There’s never been a better time, really.

Mark: But don’t buy specs and then turn around and flip. [Everyone agrees.]

Tom: Absolutely. You want it to be your primary residence, that place where you’re going to settle. The money’s out there from the banks to borrow.

Kathy: You should definitely support the local community. If you conserve too much, everything contracts.

Dave: It’s a balancing act. If it’s not going to destroy that disciplined budget you came up with, choose to buy locally and support our local economy versus buying on the Internet.

Mark: In terms of where we are and when we come out of all of this, Sean Snaith from UCF is forecasting that Ocala/Marion County will be the number one MSA (Metropolitan Statistical Area) in Florida in percentage growth between now and 2010. We know this huge bubble with the Baby Boom is coming.

We went way too fast, but that doesn’t mean that we’re not still growing. We just got a little ahead of ourselves.

Roy: That’s a real good point. Had we not had this erratic, out-of-control growth period, we would’ve been on a certain path.

Dave: To tie it back to the banks for a second, I equate us to the canary in the coal mine. Until we’re healthy, the rest of the economy is not going to get its footing. That’s why I support the bailout, to get rid of the fear.

‘A Self-Fulfilling Prophecy’

Kathy: Don’t you think this has been a reality check? Do you think it’ll make an impact?

Tom: I think people realize now that greed is not good.

Roy: Trouble is, twenty years from now when we’re all retired, people will forget what happened in 2008.

Tom: The acronym for FEAR is False Evidence Appearing Real. I think a lot of that has been driving what we’ve been talking about today. Everybody’s said it at least two or three times—fear. Hopefully, this story will alleviate some of that fear and get people looking at facts.

Kathy: Well, that’s what we’re hoping to do here.

Mark: I wish everyone in media would do what you all are doing. I think they just don’t know any better.

Kathy: Well, they’re looking for sensationalism. They think that’ll sell more.

Roy: I know, but they don’t really think about the ramification of how powerful the word is before it’s stated. Too many people in our society just read headlines.

Dean: But there’s so much media out there now, from talk radio to whole channels devoted to this sort of thing. I think what would probably be best for you all is if this got off the front page and the media stopped treating this like a sports score, where you’re tracking statistics.

Dave: It did, and it got healthier there for a little while. If you look at when earnings were coming out in July, things were horrific. Then we had a couple of natural disasters, the elections heating up, vice presidents getting chosen, and from August to mid-September, things were calm again.

Kathy: We’ve seen that with businesses panicking and overreacting.

Dave: “Who’s next?”

Roy: Yeah, that was the big headline. And then they’d try to find who to make “the next.”

Dave: Unfortunately, there are some out there still, even in Marion County. But there are other banks out there—regional banks in the Midwest—that the media’s pegged as potentially “next.” Unfortunately, they will be next.

Roy: It becomes a self-fulfilling prophecy.

Chris: I think it’s important to note that when you look at banks in Marion County, you see a lot of the same faces that have been around for a long time.

We’re here for a reason—we love our community and we give back. We may have changed our seats a couple of times, but really it’s the same people. We’re banking on Ocala, and we’re bankers in Ocala.

Dean: It’s important for our readers to know that these are local banks. They’re real people.

Tom: I think that’s the reason why we recover faster than other markets.

Dean: Well, I think we’re starting to wind down here. Anything we haven’t covered?

Dave: Wachovia did not fail. [Everybody laughs.]

Tom: We need to highly discourage storing cash in the mattress.

Mark: One of my favorite questions to ask is: “Tell me how many banks have failed this year.” You wouldn’t believe some of the numbers I get—100, 200, 300. It’s 13—and only one in Florida.

Tom: I don’t think we can fool ourselves into thinking that this thing is all over, though. Things are still going to be tough for a while—more banks will fail.

We’ll handle it.